Another set of Canadian mortgage rule changes was announced this week and these changes hurt. A lot!

When is our Federal Govt going to realize that national policy aimed at “cooling off” prices in two major markets is hurting far more people / stakeholders than it’s helping?

There’s prudent policy and then there’s crushing the life of one’s homeownership dream altogether. Here’s a collection of stories from people affected by the last policy changes: www.newruleshurt.ca

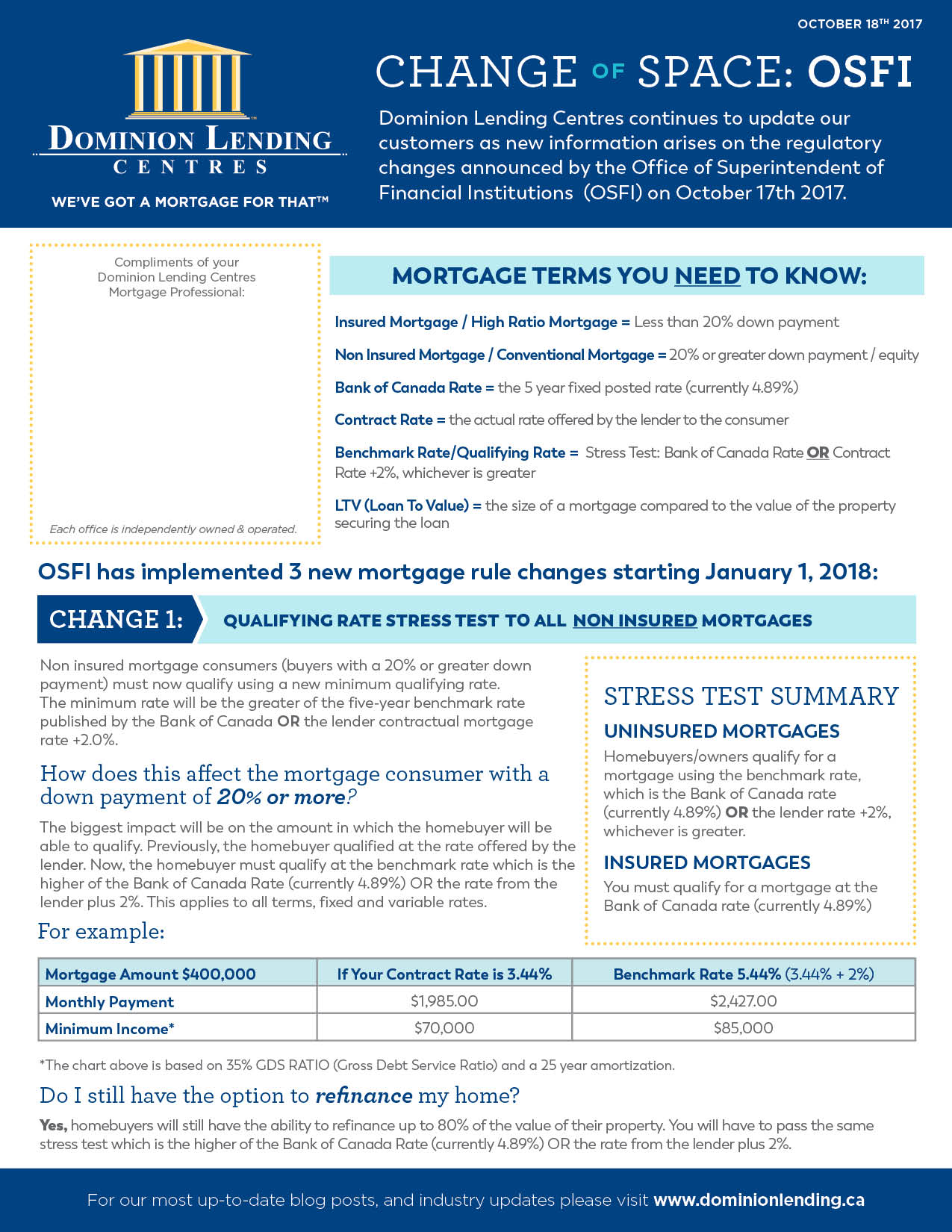

Now here we are, one year later with even more mortgage rule changes forthcoming under the guise of “prudent policy” and “avoiding US style housing crash”. A summary & descriptions of what these changes mean is posted at the bottom of this post for your reference:

I only need to point to a Canadian mortgage default rate of .30% vs 10-15% in the height of the US meltdown to see that we are not talking about the same scenario in the slightest. Let’s be honest – mortgage rule changes grab headlines and headlines become the ultimate back-pat for our elected “leaders”. I posted the the following blog in January 2017 when the first wave of policy changes were implemented http://bit.ly/StopTheMortgageMadness. And the hits just keep on coming.

In what logic should a person with a 30-50% equity position or more and strong fundamentals be held to rigid lending standards in the name of “risk”?

In what logic should a company whose business is to lend money not be allowed to decide on their own the risk they are willing to bear when lending their money for return/profit of their business?

These changes do not just affect buyers. They affect all mortgage holders. They also affect a bunch of mortgage lenders that play a VERY important role in the mortgage marketplace in Canada. There are mortgage specific (monoline) lenders that once were focussed on offering lower rates and mortgage costs while improving service levels, payment privileges, accessibility and all around lending experience for the consumer. These lenders are being bullied out of the competitive space by these government rule changes. Their competitive advantage and cost of funds is being increased dramatically by these changes and this is a direct benefit to balance sheet lending institutions IE chartered banks. Banks have no problem charging a higher rate of interest if there aren’t competitors that are able to keep rates down. They also have no problem recapturing market-share they once lost to monolines through the mortgage broker channel. The cost of mortgage financing has & will continue to rise directly due to these changes by our Federal Govt.

I thought Govt is elected to act on behalf of citizens? Sure seems like they are acting more on behalf of a handful of financial institutions better know as “The Big 5”. Maybe that’s always been the case?