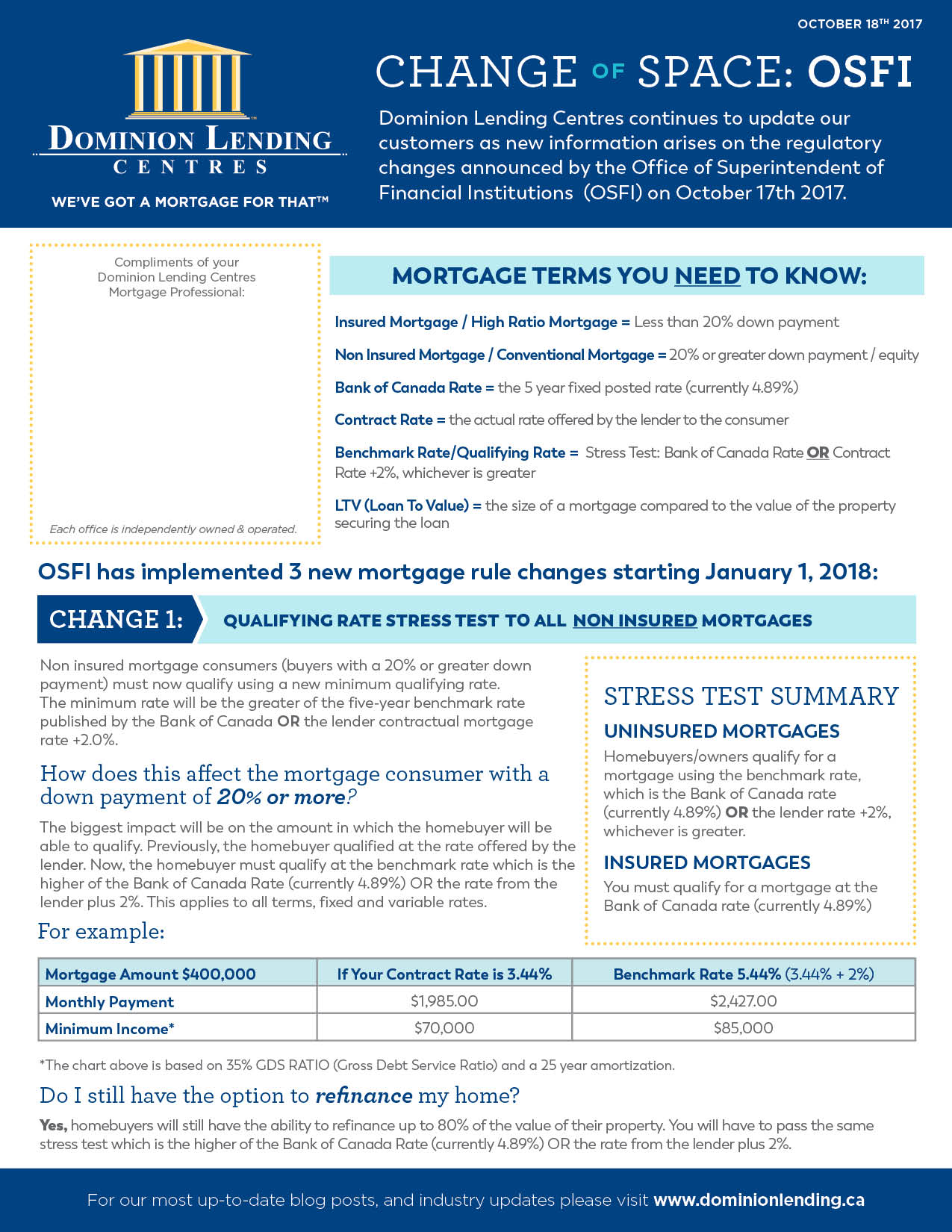

OK here’s my soapbox moment in response to the recent CMHC news

In case you missed news of this on Tuesday, CMHC announced that buying a home with less than 20% downpayment gets more expensive as of Mar 17 due to increased mortgage default insurance premiums. Now having worked as a Mortgage Professional for almost 10 years, I’m used to government & lender policy changes, credit qualification tightening and a seemingly endless number of restrictions being added to mortgage approval processes, making even the best credit candidates left to feel like they seen as untrustworthy or unable to buy a home / borrow money they know they can afford.

Up until this point, what do we do? As mortgage professionals we shrug our shoulders, gripe internally to colleagues, rip pages out of our lending policy manuals, replace them with the seventh edition of revised notes and get to updating our clients and realtors most immediately affected by the new wave of changes. That was up until this point. Up until the 2nd MAJOR government policy change announcement directly effecting mortgage borrowing in less than 3 months! At this stage I had to scream the question (through social media channels) on behalf of mortgage consumers – when is enough, truly enough?

When I read the Globe & Mail headline on Tuesday, I will be honest – 100% UNshocked, UNsurprised. Despite a CMHC article a mere few months back stating in writing according to their (likely very expensive) risk study / stress test, that CMHC was very well positioned to withstand “extreme scenarios”, we in the industry have heard rumbles of premium increases seemingly since the last premium increases. So this news didn’t get me too wound up. That was until I read the following:

“The government-owned mortgage insurer said the increases would amount to an extra $5 a month for the typical insured mortgage”

This was CMHC’s justification to a move that will cost mortgage consumer millions of extra dollars? I’m sorry but it has crossed the point of absurdity when a move like this starts to get dollarized in terms of monthly affordability by the policymaker initiating the change. That is a car / retail sales trick where you gloss over the true cost of borrowing in favor of “look at these payments. You can afford to make them right?”

What we are failing to point out is that as of March 17 (Happy St Patrick’s Day!!), consumer’s equity IE Net Worth is further eroded when purchasing a home with less than 20% down for the 3rd time in 4 years! The article points towards profitability. I’m sorry but aren’t the default insurers in place to MINIMIZE RISK to lenders not MAXIMIZE PROFITABILITY. Mortgage defaults in Canada are less than .50%. They were 10.0% in the US during the credit crisis and are still well over 10 times as high in the US as of 2015.

Here’s a novel concept when it comes to collecting premiums – make qualifying for a home a bit easier. Reduce the barriers to entry to buying a home in Canada (In US you actually get a tax advantage by owning a personal residence) and then collect your pound of flesh by having more loans under administration. Price increase doesn’t have to be the only solution to increasing revenues / assets under administration. DO A BETTER JOB, HELP MORE PEOPLE, DO MORE BUSINESS!

I can 100% GUARANTEE that if one of the private default insurers were able to say, “you know what, we feel the premiums we are charging are fair, we aren’t going to follow CMHC’s lead on this move”, the resulting influx of business flooding here vs CMHC would trump this so called prudent “Negligible” premium increase.

More laughable is that these changes charge a higher premium (respectively) to those putting MORE than 5% down? How on earth can you say that you are mitigating risk by charging a higher respective premium on a LESS RISKY loan? Mind-blowing!!

At the end of the day, when you mix less equity to start with high penalty fixed mortgage products, a historical desire to change mortgages every 3.7 years by consumers and relatively flat housing market (at least where I’m at in Alberta), buying a home sure doesn’t represent the long term sound financial strategy that it once did. If only we didn’t need a place to live.

With all of the recent regulation changes, OSFI audits & threats of sanctions or further regulation, and forthcoming costs of lender risk-sharing, one can pretty easily start to see that our ivory tower occupants sure seem hell bent on choking out whatever semblance of a dream of homeownership remains for a considerable portion of our consumers. Must be a lot of landlords in Sr Govt positions! This post doesn’t even touch on the drastic industry ramifiations and stemming from the rule changes announced in October 2016. In fact, most non-mortgage professionals would have zero knowledge of the true power shift in favor of Big Banks (away from customer) as a result of the changes as the true meaning & impact of these was seemingly disguised behind a relatively minor qualification rule change. We have already seen mortgage interest rates rising and lending options narrowed across the board as a direct result of the October changes. When competition is narrowed in any industry, the largest players (in our case, the Big Banks) have much more contol over prices (interest rates). Very soon we will likely be fielding questions to the effect of “But I am putting MORE money down, what do you mean my interest rate is higher than the person putting 5% down?” *Topic for another conversation.

I guess the point of the rant is that I LOVE MORTGAGE BROKERING** and am deeply concerned about what this seemingly non-stop barrage on our industry is going to result in for us as industry professionals and much more so the consumers that we try so hard to help every day. I have written to our MP, as I know many of my industry colleagues have as well – some with great success in engaging conversations to be relayed to Ottawa. This is important. But even more important is that consumers also start to recognize or be informed of what is going on as well and engage these same conversations; raise the same concerns that their money, long term financial health and freedom / ability to choose from a wealth of excellent non-bank lending facilities has been impeded. We need mortgage consumers to ask the same question as I did above – “When is enough, truly enough?”

**This post was initially published in an internal mortgage broker discussion forum bearing the same name. I left the line in the public article to convey the passion and care for that so many of my industry colleagues share. We are licensed professionals who do what we do with the upmost priority being placed on saving people money & helping them achieve financial goals. The ability to do so has again been hampered by unnecessary government intervention.